Confidence Remains Strong Amid Increasingly Mixed Market Signals

Results from our latest monthly survey across lumberyards, one-step dealers, homebuilders, and contractors point to a market that remains fundamentally optimistic—though not without emerging caution.

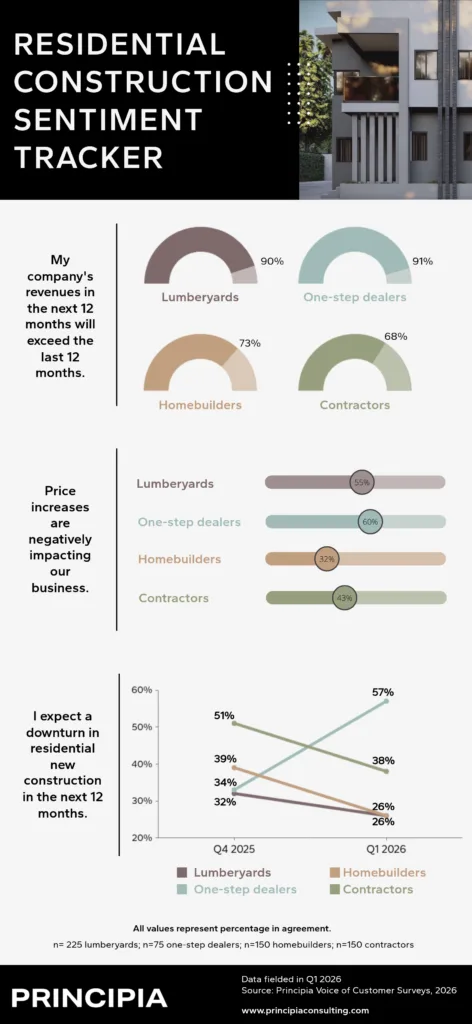

Across the supply chain, revenue confidence is strong. The majority of lumberyards (90%) and one-step dealers (91%) expect revenues in the next 12 months to exceed the prior year. While optimism softens slightly downstream, it remains solid, with 73% of homebuilders and 68% of contractors expecting revenue growth. This underscores continued demand and resilience, even as the industry navigates a more complex operating environment.

At the same time, pricing pressures remain a persistent challenge—particularly for distributors. More than half of lumberyards (55%) and one-step dealers (60%) say price increases are negatively impacting their business, compared to a smaller but still meaningful share of contractors (43%). Homebuilders appear least affected, with just 32% citing negative impacts.

Looking ahead to the demand for residential new construction, sentiment is uneven and shifting. In Q4 2025, concerns about a downturn were most pronounced among contractors (51%), while other groups remained more measured. By Q1 2026, expectations diverged further: downturn concerns eased among lumberyards and homebuilders (both at 26%), but rose sharply among one-step dealers (57%). This shift highlights differing vantage points across the value chain and signals a more fragmented outlook for residential activity as the year progresses.

Overall, the data tells a nuanced story—strong revenue confidence anchored by ongoing demand, counterbalanced by pricing pressure and selective concern about future construction activity. For industry leaders, the message is clear: opportunity remains, but agility and close attention to customer signals will be critical in the months ahead.