Commercial Door Demand by Building Type

Why Interior, Exterior, and Overhead Doors Tell Very Different Market Stories

At first glance, commercial door demand can appear evenly distributed across building types. When all door types are combined, most major commercial sectors—education, office, retail, healthcare, industrial—seem to share the market relatively evenly.

But that top‑line view masks the real story.

Once door demand is segmented by door type—interior, exterior, and overhead—a much clearer and more actionable picture emerges. Different buildings use doors for fundamentally different purposes, and those functional differences drive where demand is concentrated, where it is fragmented, and where true specialization exists.

This is where granular demand modeling matters—and where manufacturers gain insight that total market numbers alone cannot provide.

One Market, Three Very Different Demand Profiles

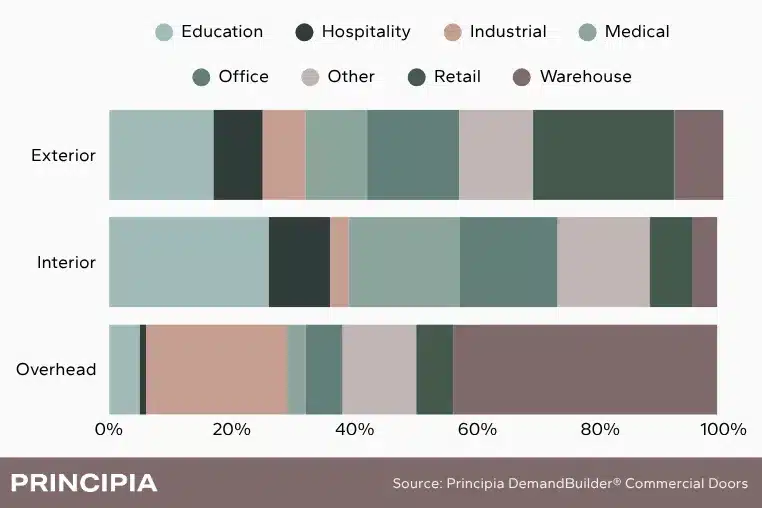

Figure 1 compares overall commercial door demand by building type with segmented demand for interior, exterior, and overhead doors. The contrast is immediate: while the total market looks balanced, each door category has its own demand hierarchy by building type.

For manufacturers, this distinction is critical. Product opportunity is defined less by total construction activity and more by how doors are used within each building environment.

Figure 1: Commercial Doors by Building Type, 2025

Exterior Doors: Where Volume Meets Visibility

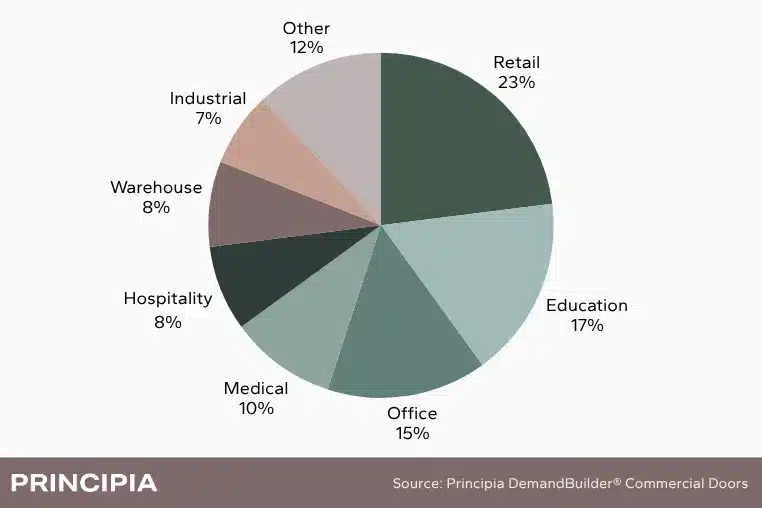

When exterior doors are isolated, the market shifts decisively toward retail. Storefronts, shopping centers, and mixed‑use developments collectively account for the largest share of exterior door demand—surpassing education and office buildings. Figure 2 shows commercial doors demand by building type for exterior doors.

This demand is driven by design and function:

- High visibility requirements tied to branding and tenant experience

- Frequent entry and egress for customers and staff

- Multiple access points per building

Figure 2: Commercial Doors by Building Type — Exterior, 2025

Education and office buildings still represent meaningful demand, reflecting campuses and multi‑tenant complexes, but retail’s dominance underscores a key point:

Exterior door demand tracks public interaction, not square footage.

What this means for manufacturers:

Manufacturers focused on exterior systems benefit from targeting building types with high visitor traffic rather than simply high build volume. Principia’s data allows exterior door demand to be sized by building type, redevelopment activity, and regional concentration—supporting smarter prioritization of retail‑heavy markets and customers.

Interior Doors: The Backbone of Institutional Demand

Interior doors tell a very different story.

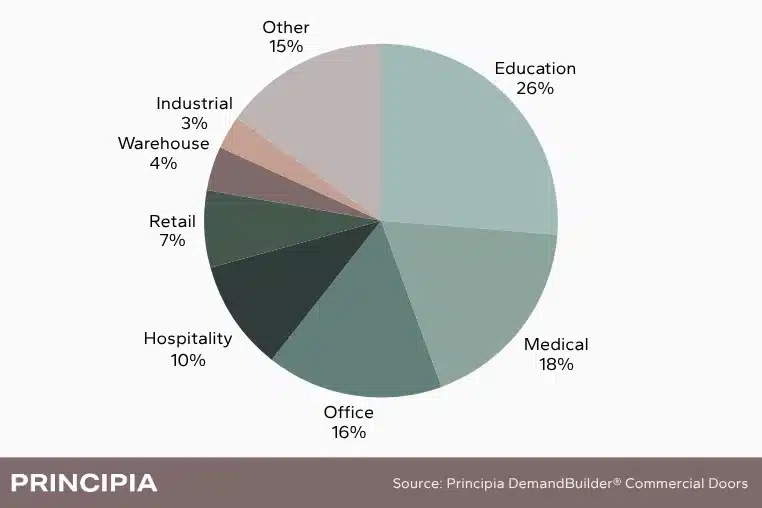

Education and healthcare buildings dominate interior door volumes, together accounting for nearly half of all interior units installed. Office buildings follow closely behind.

The driver here is spatial design. Schools and hospitals are highly compartmentalized environments—classrooms, offices, labs, patient rooms, treatment areas, and corridors—all of which require separation for:

- Privacy

- Safety and code compliance

- Acoustics and infection control

Office buildings also generate substantial interior demand, though typically with fewer doors per square foot than institutional facilities.

Interior door demand is shaped by:

- Room count and space density

- Regulatory and accessibility requirements

- Ongoing renovation and reconfiguration cycles

Figure 3 shows commercial doors by building type for interior doors.

Figure 3: Commercial Doors by Building Type — Interior, 2025

What this means for manufacturers:

For interior door suppliers, opportunity is concentrated in institutional buildings where door counts scale with functional complexity, not building size. Our demand model enables manufacturers to isolate these segments and evaluate opportunity driven by renovation versus new construction.

Overhead Doors: A Concentrated, Specialized Market

The most dramatic divergence appears in the overhead door category.

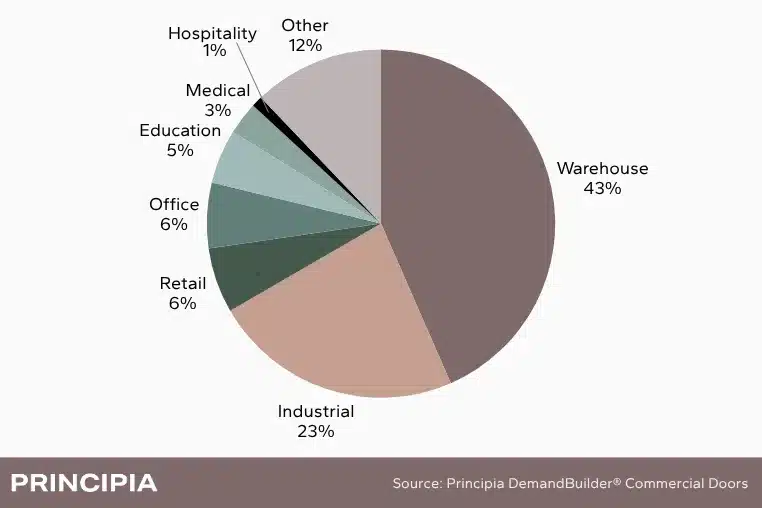

Here, warehouses and industrial buildings dominate, accounting for roughly two‑thirds of all overhead door demand. No other door type shows this level of concentration.

Overhead doors are purpose‑built assets, closely tied to:

- Equipment and vehicle access, not occupant movement

- Logistics and distribution workflows

- Manufacturing and material handling

Figure 4: Commercial Doors by Building Type — Overhead, 2025

Unlike interior and exterior doors, overhead systems are not broadly distributed across commercial buildings. They are tightly linked to function‑specific environments—particularly those connected to supply chains.

What this means for manufacturers:

Overhead door demand is highly targeted. Success depends on accurately sizing logistics‑driven construction, understanding warehouse typologies, and tracking sector‑specific investment trends. Principia’s data allows manufacturers to separate truly addressable demand from broader commercial activity—avoiding overestimation and sharpening focus.

The Strategic Takeaway: Relevant Opportunity vs. Total Opportunity

Viewed together, these demand profiles reveal a critical insight:

The role a building plays determines door demand—not just its size or construction value.

- Exterior doors highlight public interaction

- Interior doors reflect organizational complexity

- Overhead doors track the movement of goods

By separating door demand into interior, exterior, and overhead categories—and then evaluating each by building type—manufacturers gain clarity on:

- Where demand is concentrated

- Where it is diffuse

- Where specialization matters most

This approach moves beyond total market sizing to identify relevant opportunity—the segment of demand that truly aligns with a manufacturer’s products, customers, and go‑to‑market strategy.

How Manufacturers Use This Data

Principia’s commercial doors coverage enables manufacturers to:

- Size and prioritize TAM by product type and building segment

- Align portfolios with the building types that matter most

- Identify whitespace and under‑served niches

- Support segmentation, sales planning, and resource allocation

- Tailor insights for different internal initiatives—strategy, marketing, M&A, or sales enablement

The ability to cut demand by door type × building type is not just analytical detail—it’s a competitive advantage. It allows manufacturers to replace broad assumptions with focused, defensible market intelligence.